Banks don't need watchdog!

Bad loans are plaguing the banking system of India. Though the central government has been talking about measures to address this growing menace, very little has happened in spirit. While disclosing willful defaulters is the need of the hour, banks, particularly in the public sector need to put in place checks and balances in disbursing loans and a thorough due diligence. Constant auditing of accounts can send early alerts of accounts that may turn into non-performing assets.

Reserve Bank of India (RBI), the banking sector watchdog, which is supposed to know the health of the banks, should save them in time rather than waiting to give them the death certificate. Criminal action against willful defaulters is the only solution, experts point out. Prime Minister Narendra Modi’s government in August last year pledged to pump in Rs70,000 crore ($10.2 billion) into State-run banks through four years to March 2019 as part of a major banking reforms plan.

Lenders were expected to raise an additional Rs1.1 trillion from the financial markets. But an increase in provisions for bad loans in a RBI-directed balance sheet clean-up exercise has sent several banks into losses, hammering their stock prices and limiting their ability to secure external funding. The Supreme Court on Tuesday directed the RBI to provide a list of companies which are defaulters of bank loans of over Rs 500 crore, in sealed covers, while expressing serious concern over the rise in bad loans.

The apex court also asked the RBI to provide by end of March the list of companies whose loans have been restructured under corporate debt restructuring schemes. C H Venkatachalam, general secretary of AIBEA, told Metro India, “After the PIL has been filed in 2005 against bad loans by Centre for Public Interest Litigation (CPIL), the Supreme Court has now given a directive to RBI to furnish a list. Instead of presenting the list in sealed covers, it should have been transparent but the court taking cognisance of the matter is a key signal. Bad loans are killing the banks.

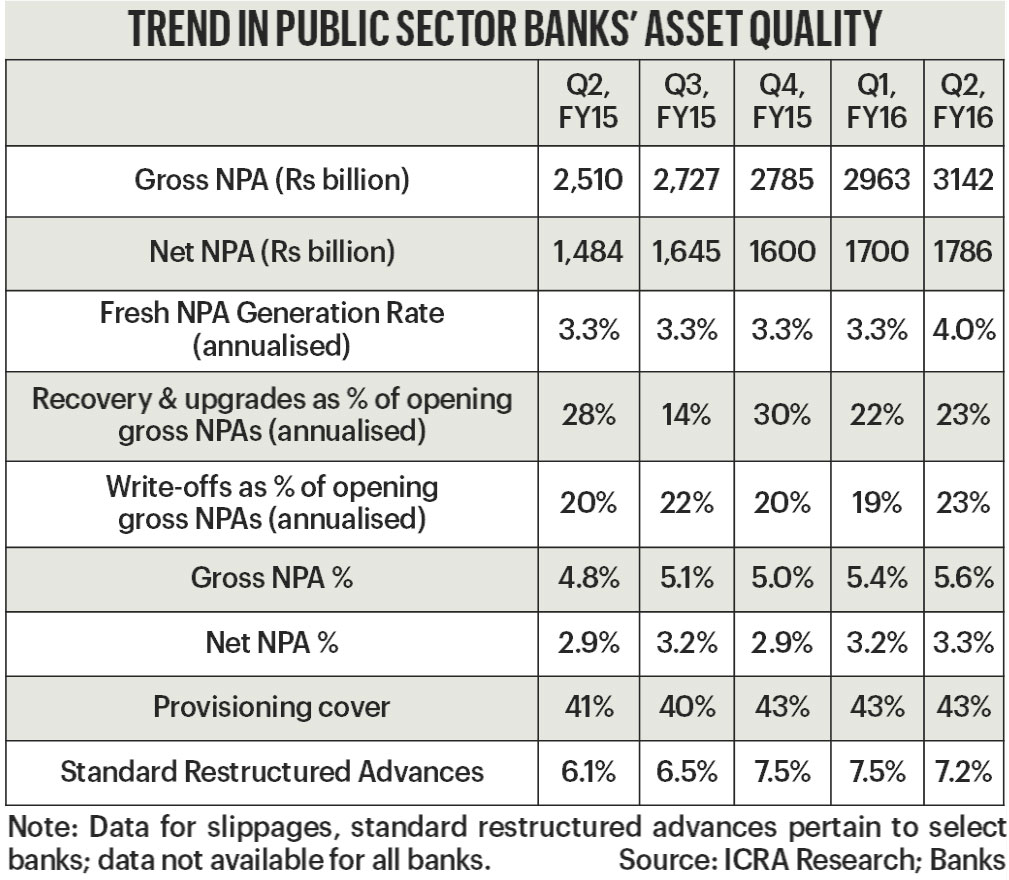

Banks are bleeding, suffering and are continuously in losses.” Suggesting measures to address bad loans menace, he said, “The list of defaulters should be kept in public domain, recovery laws should be amended and fast track recovery tribunals should be set up particularly to deal with high volume defaults. The bad loans in India account to almost Rs 3 lakh crore while the restructured loans also equal that amount. Banks are facing a significant loss of interest on these loans.”

Nationally, 29 State-owned banks had written off Rs 1.14 lakh crore of bad debts between the financial years 2013 and 2015. Punjab National Bank this week declared the promoter of defunct Kingfisher Airlines, Vijay Mallya, as a willful defaulter. M Devaraja Reddy, president, Institute of Chartered Accountants of India (ICAI), observed, Indian banks need good independent auditors who could put a check on NPAs. Also banks are getting only 20 per cent of their branches audited and if every branch is audited then there could be control on loan disbursement.

Lack of proper auditing is one of the reasons for the rising NPAs. Santanu Mukherjee, Managing Director, State Bank of Hyderabad, told Metro India recently, “Iron & Steel, Power, Infrastructure, Textiles, Construction, Metals are facing stress. Many companies in these sectors are affected by the overall economy. Iron and Steel have significant exposure. Two SBH accounts from this sector alone account for Rs 700 crore. The net Non Performing Assets (NPAs) stood for the first nine month of the financial year at Rs 2,894 crore.”

Unlike the past when banks could hide defaults, new rules mandate that banks set aside funds for potential losses to avoid increasing of risk when loans actually turn into non-performing assets. A loan is classified as an NPA if an installment remains unpaid for 90 days. Vikas Singh, president, Crux Management Services, said, “Almost 80 per cent of the prospective bad loans can be controlled at appraisal stage, while with thorough monitoring banks can avoid adding them up.

Also Indian banks do not give loans that suit the tenure of the borrower’s project-for instance, a toll road project with 50 year agreement getting only a five-year loan will not help the borrower to repay the principal on time. Iron sector also is a problem area. Banks need to thoroughly monitor the account movement in advanced stages of becoming a bad loan.” All India Bank Employees’ Association (AIBEA) is planning a massive rally to Parliament involving 30,000 bank employees on March 14, demanding stringent measures to revive banking system including recovery of bad loans.

AIBEA is gathering one lakh signatures in support of its initiative to turn public sector banks into people oriented banks. "The RBI acknowledges that there are 7,035 wilful defaulters involving about Rs 58,800 crore. Why can't criminal action be taken against these defaulters? People’s money is given to them as loans. When corporates do not share profits with banks, how can they not repay their loans to banks when they incur losses? ," asked Venkatachalam.

-

Related News

- UIMI Technologies unveils solar chargeable power bank

- Sanjeevani from Exide Life insurance

- Orbis launches comic strips for children

- App to give virtual trial room and in-store shopping experience

- Woman creates buzz in startup ecosystem

- India raised Rs 65,789 cr from spectrum auction

- Indsur Global puts Rs 150-cr expansion plan on hold

-

More from Metro India